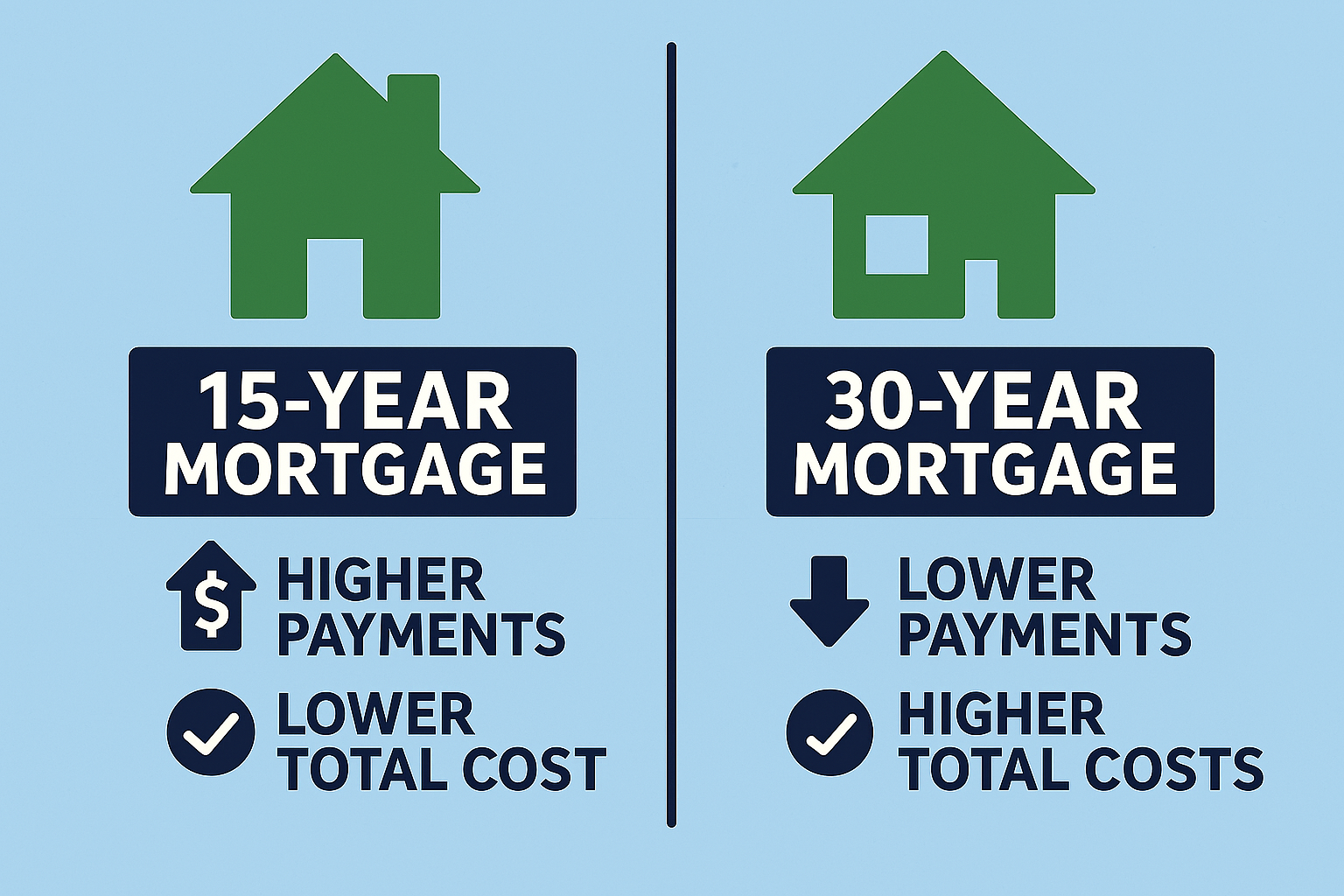

A 15-year mortgage and a 30-year mortgage seem like they’re miles apart, but there are many different advantages of going one path over the other. Financial gurus like Dave Ramsey recommend a 15-year fixed-rate mortgage over a 30-year.

But is the 15-year mortgage the best choice? Let’s break down the math and review four different categories to see which option is best.

Consideration 1: Interest Rates

Typically, we see lower interest rates for a 15-year mortgage over a 30-year rate. As of July 2025, the interest rate for a 15-year loan is around 5.87% versus 6.74% for a 30-year.

Winner: 15-year Mortgage

According to freddiemac.com, mortgage rates for the last 10 years have always been lower for a 15-year loan

Consideration 2: Monthly Costs

While 30-year mortgages have a higher interest rate, the principal balance is spread over 30 years, rather than 15. This means that the monthly payment is usually much smaller.

Scenario 1

Home cost: $400,000

10% down ($40,000)

Interest Rate 6.74% (30-year) & 5.87% (15-year)

$0 fees and taxes (for calculation purposes)

30-Year: For a $360,000 loan, we are looking at around $2,332.56 in monthly mortgage payments. For this loan, you would need to assume some PMI, but we’re ignoring it for now.

15-Year: For the same $360,000, but for 15 years, we are looking at a monthly payment of around $3,012.66 a month.

For this scenario, the mortgage payments are $680.10 (+29.2%) more for a 15-year mortgage.

Let’s try another scenario, but change some numbers around.

Scenario 2

Home cost: $300,000

5% down ($15,000)

Interest Rate 6.74% (30-year) & 5.87% (15-year)

PMI 1%

$200/month for Insurance

$2000/year for property tax

30-Year: For a $285,000 loan, we are looking at around $2,450.78/month. The extra fees for private mortgage insurance (1%), plus taxes and insurance, bring the cost way up.

15-Year: For the same loan amount, fees and taxes, but over 15 years, the mortgage payment is $2,989.19.

We see in a realistic scenario, the mortgage payments for a 15-year loan is still higher than a 30-year, around $538 more. That’s only a 22% increase higher than a 30-year loan.

Winner: 30-year mortgage

Consideration 3: Interest Paid

Let’s break down the interest payments for those two above scenarios.

Scenario 1

$360,000, 30-year loan at 6.74%

Total interest paid over 30 years is $479,722.

$360,000, 15-year loan at 5.87%

Total interest paid over 15 years is $182,278.

A 30-year loan would cost $297,444 more (+163.2%) in interest costs.

Scenario 2

$285,000, 30-year loan at 6.74%

Total interest paid over 30 years is about $379,780.

$285,000, 15-year loan at 5.87%

Total interest paid over 15 years is about $144,303.

A 30-year loan in scenario 2 would cost $235,477 more (+163.2%) in interest costs.

For the same loan in both scenarios, the interest payments are significantly higher for a 30-year mortgage.

Winner: 15-year mortgage

Consideration 4: Total Payments

Let’s continue with our two scenarios and calculate the total payments for each.

Scenario 1

$360,000, 30-year loan at 6.74%

Total payments: $839,721.83 (+233.3% more than the loan)

$360,000, 15-year loan at 5.87%

Total payments: $542,278.53 (+151% more than the loan)

In this scenario, the total payments for a 30-year mortgage are $297,443.30 more than a 15-year mortgage.

Scenario 2

$285,000, 30-year loan at 6.74%

Total payments: $826,704.79 (+290% more than the loan)

$285,000, 15-year loan at 5.87%

Total payments: $505,041.34 (+183.7% more than the loan)

In this scenario, the total payments for a 30-year loan are $321,663.45 more than a 15-year mortgage.

Winner: 15-year mortgage

So What’s the Right Choice?

15-year mortgages win 3/4 of the main considerations. We can see that anyone who decides to buy a home should choose a 15-year mortgage if they are simply trying to spend the least amount of money in the long run. A 30-year loan will cost you hundreds of thousands in interest payments.

However, the 15-year loan looses out to monthly payments in a 30-year mortgage, and when it comes to personal finances, a monthly budget is extremely important. Are you able to or willing to pay $750-$1500 extra a month to know that you might save yourself $300,000-$500,000 over 30 years?

Some questions you should ask yourself:

- How much can I afford on rent/mortgage each month?

- How much will I have after my monthly payments?

- Do I want to live in this house forever?

- Is my credit rate strong?

- How much money can I put down?

We can see that the clear choice for the long run is a 15-year mortgage. You spend significantly less, and you are out of debt much sooner. This is why people like Dave Ramsey tell you to pick a 15-year mortgage. If you can afford to put a good down payment towards the principal cost, plan on living in the house for several years, and can easily afford your monthly payments, then a 15-year mortgage is right for you. However, if you can’t afford the extra monthly payments right now, you can make additional payments in the future towards your home when your income increases and still choose a 30-year mortgage.